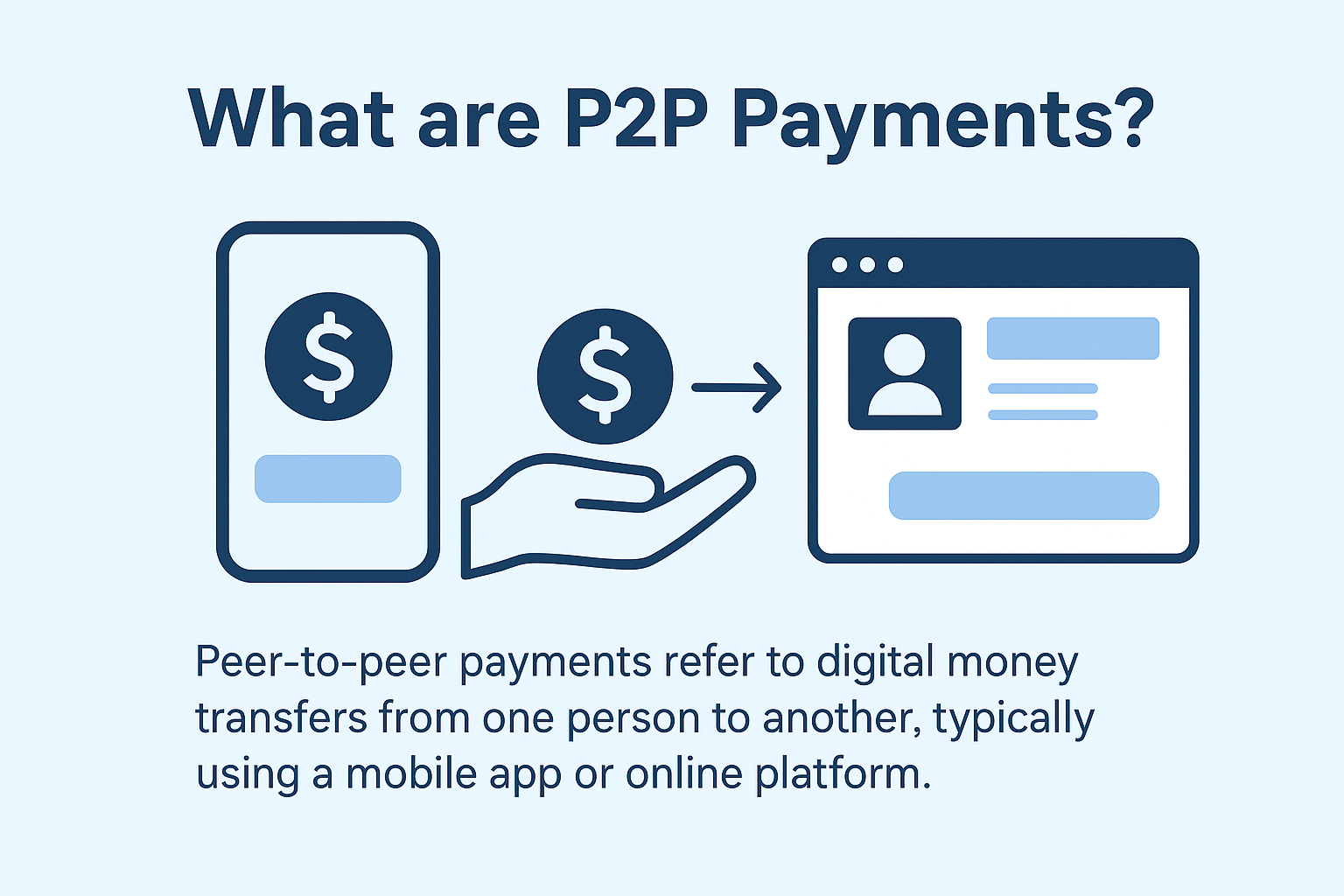

Peer-to-peer (P2P) payments refer to digital money transfers from one person to another, typically using a mobile app or online platform. Instead of going through cash or physical checks, individuals can send funds directly to friends, family, or acquaintances with just a few taps. Popular P2P platforms include services such as Venmo, Cash App, PayPal, Zelle, and others. These are part of modern payment processing solutions that make sending and receiving money fast, seamless, and largely frictionless.

P2P payments are especially useful for splitting bills, sharing rent, reimbursing someone, or sending gifts. Because they rely on linked bank accounts, debit/credit cards, or digital wallets, there’s no need for physical exchange of cash. Over the past few years, P2P payments have seen explosive growth, driven by smartphone adoption, digital banking trends, and a preference for cashless transactions.

How Does P2P Work?

Here’s a simplified breakdown of how P2P payments function:

- Registration & Setup: A user signs up for a P2P payment app and links their bank account, credit card, or debit card.

- Choose a Recipient: The user selects a contact or enters the recipient’s identifier (email, phone number, username, or QR code).

- Enter an Amount: The sender specifies how much money to send and may add a note (e.g., “Dinner split”).

- Authorize the Payment: The user confirms the transfer, often via PIN, biometric data, or two-factor authentication.

- Settlement: The app processes the transaction. Funds may move instantly (or nearly so) or take a little time, depending on how the sender funded the payment and how the recipient withdraws the money.

- Notification: Both sender and recipient typically receive notifications once the transaction succeeds.

Behind the scenes, P2P apps act as payment processing solutions, handling the flow of money, ensuring security, verifying identities, and sometimes applying fees depending on funding methods.

How Safe and Secure Are P2P Payments?

P2P payment platforms are generally quite secure, but they’re not immune to risk. Here’s how safety is handled, and where potential vulnerabilities lie.

- Encryption and Authentication: Most P2P services use encryption to protect data in transit. They also offer multi-factor authentication (MFA) or biometrics, which adds a layer of security.

- Fraud Detection: Many platforms invest in fraud detection systems using AI to flag suspicious transactions. According to a market report, nearly 48% of providers are investing in AI-driven fraud detection.

- Irreversibility: One important security limitation: once a P2P payment is made, it often can’t be reversed easily. If funds are sent to the wrong person or a scammer, getting that money back can be difficult.

- Fraud Risk Statistics: According to a recent tracker, 27% of firms using real-time payments reported increased fraud tied to faster payments in 2023.

- Consumer Awareness Needed: Because P2P payments are so fast, users may act quickly without double-checking details. Scammers sometimes exploit this through “authorized push payment” (APP) fraud, social engineering, or by impersonating someone trustworthy.

In short, P2P payments are safe when used carefully, but users need to be aware of scams and double-check recipient details before sending money.

How Much Do P2P Payments Cost?

Costs for P2P payments vary depending on how funds are sent, the app used, and whether the transfer is domestic or international. Here’s a breakdown of common fees:

- Instant Transfers: Many P2P apps offer “instant” or “fast” transfer options so that the recipient gets funds quickly, often for a fee. These fees may be a flat rate or a percentage of the transfer.

- Debit or Credit Card Fees: If you fund a P2P payment with a credit card, expect to pay a higher fee. Debit-card–funded transfers might have lower or no fees, depending on the provider.

- International Fees: Sending money across borders can involve currency conversion fees or international transaction charges. These may be significantly higher than domestic P2P transfers, depending on the provider and the currencies involved.

Because P2P payment platforms are part of broader payment processing solutions, how they charge and structure their fees reflects typical transaction‑processing business models.

P2P Payment Benefits

Why do so many people and small businesses like P2P payments? Here are some of the main advantages:

- Instant Payments: One of the biggest draws is speed. P2P platforms often facilitate near real-time transfers, especially for small amounts.

- Cost-Effective: For personal transfers, P2P payments are often cheaper than traditional bank wire transfers or check payments. Some transfers are free or have minimal fees.

- Digital Invoicing & Payment Requests: Many P2P apps allow users to request money, send invoices, or split bills electronically, making it easy to manage shared expenses.

- Convenience & Accessibility: With a smartphone, users can send or receive money anytime, anywhere, a big plus for on-the-go or remote users.

- Part of Payment Processing Solutions: As part of modern payment processing ecosystems, P2P payments can integrate with digital wallets or broader fintech services, offering flexibility and convenience.

P2P Payment Cons

Despite the advantages, P2P payments aren’t perfect. Here are some of the downsides:

- Not Suitable for Large Businesses or B2B: P2P apps typically lack the invoicing, purchase order, and reconciliation features that larger businesses require. They’re made for individuals splitting costs, not for enterprises sending large or recurring B2B payments.

- Limited Functionality / Integrations: Some P2P platforms don’t integrate well with accounting systems, ERP software, or merchant tools, making them less useful for businesses beyond peer-to-peer transfers.

- Availability Limitations: P2P payment apps and features are not universally available. In some countries or regions, regulatory, banking, or infrastructure barriers limit access.

- Fees May Apply: As discussed, while some transfers are free, others carry fees, especially instant transfers, credit card funding, or cross-border payments.

- Not a Bank: P2P services are not banks. They may not provide savings accounts, interest, deposit insurance, or full customer protections that traditional banks offer.

Alternatives to P2P Payments

If P2P doesn’t meet your needs, there are other ways to move money:

- Direct Wire Transfers: Traditional banks allow wire transfers for domestic or international payments. Wires typically support large amounts, but fees may be higher, and settlement times longer.

- Writing a Cheque: Though less common today, cheques (or checks) remain an option. This method is useful for formal payments, especially when a paper trail is needed, but it’s slower and requires physical handling.

- Money Orders: These are prepaid payment instruments that you can use when you don’t want to carry cash. Money orders are more secure than cash, but they may involve convenience‑store or post‑office fees, and processing times are slower compared to digital P2P.

Conclusion

P2P payments are a powerful and increasingly popular payment processing solution for everyday money transfers. They offer convenience, speed, and simplicity, making them ideal for splitting bills, sending small amounts, and handling personal transactions. However, they also come with trade-offs: they’re not built for large-scale business operations, they may carry fees depending on how you fund payments, and once money is sent, it may be difficult to reverse.

As global adoption surges, with experts projecting significant market growth in the coming years, P2P systems will likely become an even more central part of how we exchange money. (But users should always stay alert to fraud risks, verify details before sending funds, and choose the right tool (P2P or otherwise) based on their payment needs.