Mobile payments have become deeply embedded in daily life, and one technology in particular, NFC (Near-Field Communication), is powering much of the contactless experience you see at stores, cafés, transit gates, and more. But what exactly are NFC mobile payments, how do they work, and what should you watch out for in 2025? Let’s walk through it, step by step.

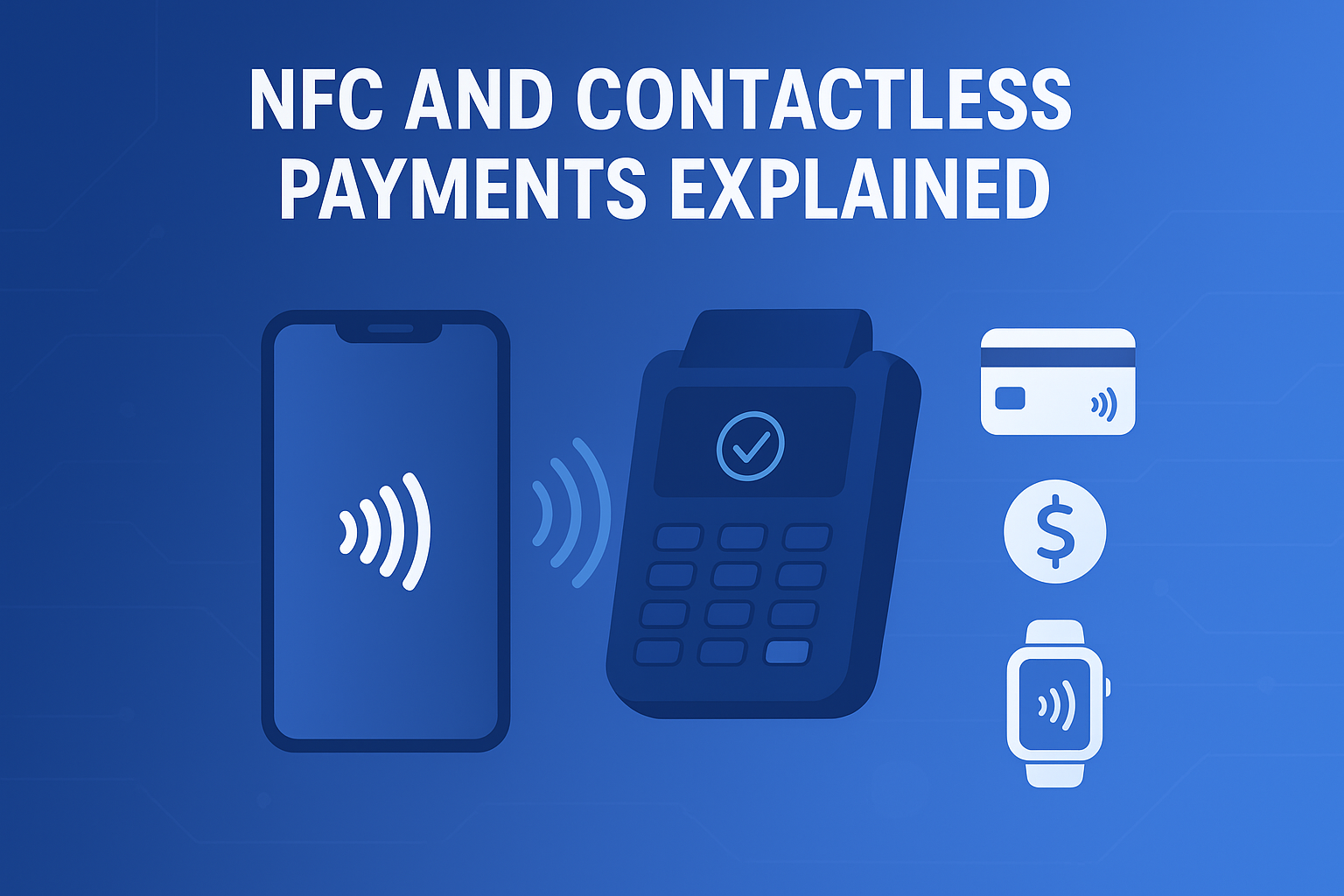

What Are NFC Mobile Payments?

In simple terms, NFC mobile payments let you pay using your smartphone (or another NFC-enabled device) by tapping or bringing it close to a point-of-sale (POS) terminal. The “tap to pay” behavior is possible thanks to NFC, a short-range wireless technology (radio frequency) that allows two devices to exchange data when they are very near each other (usually within a few centimeters).

You may already use it in wallets like Apple Pay, Google Pay, Samsung Pay, or other digital wallet apps. Under the hood, though, this fits into the broader category of mobile payment technologies, and it’s part of the growing ecosystem of payment processing solutions today.

By 2025, NFC and contactless payments are expected to dominate how people pay in physical stores. For example, the contactless payment market is projected to grow from $57.85 billion in 2024 to $70.08 billion in 2025.

These shifts make NFC mobile payments a must-know for consumers, merchants, and anyone involved in payment infrastructure.

How Does NFC Work for Mobile Payments?

Let’s break down what typically happens in a smooth NFC mobile transaction. The flow often looks like this:

A User Opens Their Digital Wallet

Your smartphone (or smartwatch) has a wallet app (Apple Pay, Google Pay, etc.) that you’ve set up beforehand with your payment cards, account credentials, etc.

The Digital Wallet Authenticates Identity

Before the payment can be triggered, the wallet confirms your identity using a PIN, fingerprint, face recognition, or another authentication method.

A POS terminal Initiates and Processes Payment

The merchant’s NFC-enabled POS reads the signal from your device, communicates with the payment network, and requests authorization.

The Customer Completes The Transaction

Once the backend systems validate everything (funds, tokens, fraud checks), the transaction is confirmed, and the payment completes, typically in under a second or two.

Let’s unpack a bit more detail:

- The communication between your device and the POS terminal is short-range (a few centimeters), limiting the possibility of unauthorized interception.

- Your actual card number (Primary Account Number, PAN) is not directly exposed; instead, a token or surrogate value is used. This is part of the security measures.

- The transaction passes through the usual payment infrastructure (issuers, acquirers, networks) just like a regular card payment, but with extra security layers.

This flow is a typical implementation of payment processing solutions designed for NFC/mobile channels. It is one form of mobile payment technologies in operation.

Key NFC Mobile Payment Security Features

Security is a major concern whenever money is involved. NFC mobile payments lean on several layers of protection. Here are the most important:

1. Advanced Encryption

Data exchanged between your device and the POS is encrypted, so eavesdroppers can’t easily decipher it. The radio link is protected, and underlying network communications also use strong cryptography.

2. Credit Card Tokenization

Instead of sending your real card number, your wallet converts it into a token, a randomized surrogate number valid only for that transaction (or a limited set of transactions). Even if an attacker intercepts it, it’s useless beyond that context.

According to Coinlaw, 89 % of NFC-based payments globally are secured via tokenization as of 2025.

3. Biometric Verification / Device Authentication

Before initiating a payment, your wallet usually demands authentication via fingerprint, face recognition, or passcode. This verifies “you” are approving the transaction. Many wallets won’t even let the NFC radio activate unless the user has satisfied that step.

4. Communication Proximity / Short Range

Because NFC works only at very close distances, the opportunity for someone distant to intercept or “sniff” the connection is greatly reduced. The physical requirement that devices must be very close adds a built-in guardrail.

In addition to these, other layers exist (e.g. secure elements in the device, Trusted Execution Environments, transaction limits) to bolster safety.

Of course, no system is perfectly risk-free. Researchers continue to examine cyber threats and possible attack vectors in NFC systems. But for most day-to-day usage, these security measures make NFC mobile payments safe and resilient.

Benefits and Challenges of NFC Mobile Payments

Every technology has pros and cons. Below is a balanced look at what NFC mobile payments offer, and where they still struggle.

Benefits

Speed & Convenience

Tap and go, no fumbling for cards or entering PINs (in many cases). Checkout is faster, which is appealing for both consumers and merchants.

Reduced Friction & Better Experience

Because you already carry your phone, it’s easier to initiate payments than pulling out cards, cash, or even dealing with QR code scanning. This helps improve user satisfaction and reduces cart abandonment.

Stronger Security Posture

With encryption, tokenization, and user authentication, NFC mobile payments can offer better security than traditional magnetic stripe or even chip-based methods.

Better Data & Integration Opportunities

Merchants can integrate loyalty, rewards, receipts, and analytics more tightly with mobile wallet systems and payment processing solutions.

Offering NFC acceptance is a differentiator within mobile payment technologies ecosystems.

Supports Small Merchants & Newer Business Models

Technologies like “Tap to Phone” (turning a smartphone into a virtual POS via NFC) are democratizing payments for small sellers. Visa reported a 200 % year-over-year growth in Tap to Phone adoption in early 2025.

Growth & Scale

NFC mobile payments are part of the broader shift toward digital payments. The digital payment market is expected to reach US$32.07 trillion by 2033 (starting from ~$10.18T in 2024).

Challenges & Limitations

Infrastructure & Hardware Costs

Merchants need NFC-capable POS terminals. In regions where older machines are prevalent, upgrading is costly and logistically complex.

Device Compatibility/Fragmentation

Not every smartphone or wallet supports NFC payments. Differences in OS, hardware, and wallet providers can limit reach.

User Trust & Adoption Barriers

Some users are still hesitant about mobile payments due to security fears or unfamiliarity.

Token Lifecycle & Network Dependence

Tokenization systems depend on robust backend network infrastructure and coordination among issuers, acquirers, and wallet platforms.

Edge Security Threats & Relay Attacks

While proximity protects against many risks, more sophisticated adversaries can try relay attacks or device impersonation. Researchers continue to study mitigation strategies.

Privacy and Data Concerns

Because mobile wallets and NFC payments are digital, there is more behavioral data collected, which raises privacy questions.

Regional Regulation/Compliance

Data protection (e.g. GDPR), financial regulations, KYC/AML constraints, and standards vary by country. These regulatory overheads affect adoption, especially in cross-border contexts.

Fallback/Offline Constraints

In poor connectivity environments, or when tokens expire or systems are down, fallback methods may be needed, complicating the experience.

While the advantages often outweigh the challenges, those obstacles must be addressed, especially for merchants and payment solution architects.

Conclusion

By 2025, NFC mobile payments will no longer be just a “nice-to-have” feature. They are core to modern payment processing solutions and form a critical pillar of mobile payment technologies overall. The speed, security, and consumer acceptance make it a go-to channel for in-person payments.

If you’re a business considering adoption:

- Ensure your POS hardware supports NFC (and software is kept up-to-date).

- Work with providers whose payment processing solutions support tokenization, fraud management, analytics, and wallet integrations.

- Educate staff and customers so they trust and feel comfortable using NFC payments.

- Monitor regional regulations (data protection, financial compliance) to ensure your systems remain legal and secure.

- Plan for fallback scenarios (e.g., offline mode) in case connectivity or token systems fail.

If you’re a consumer, keep your wallet app and phone OS updated, use biometric protection, and only use trusted apps. NFC mobile payments are generally safe and convenient, but vigilance always helps.