In today’s fast-paced digital world, handling financial transactions has become more seamless than ever. Whether you’re shopping online, paying utility bills, or transferring funds, electronic payment systems make these processes smooth, secure, and instant. These systems have revolutionized how we exchange money, providing both individuals and businesses with efficient payment processing solutions that save time and reduce dependency on cash.

What Is an Electronic Payment System?

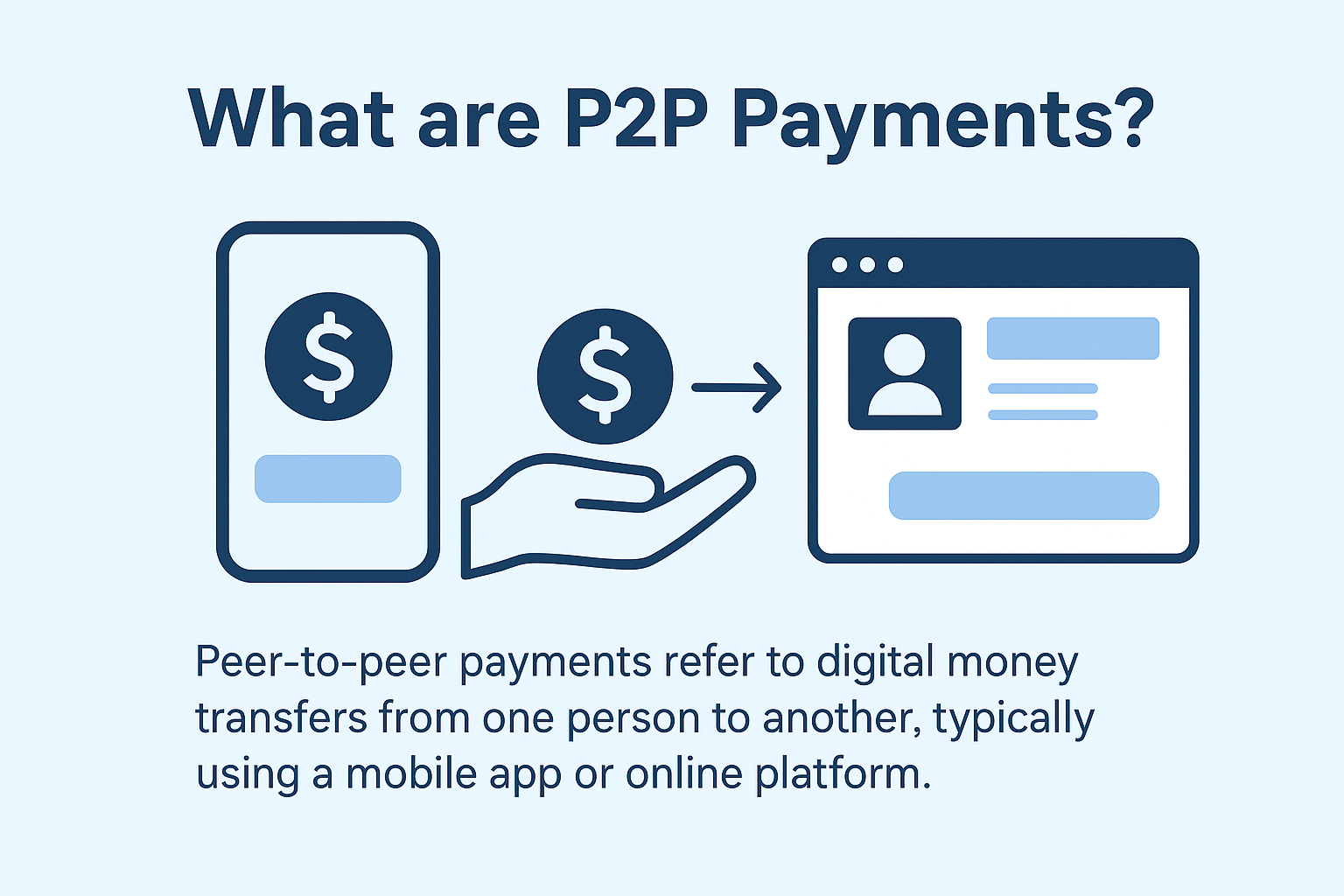

An electronic payment system refers to a digital platform that enables the transfer of funds between parties through electronic devices or online networks. Unlike traditional payment methods such as cash or checks, electronic payments rely on the internet, banking networks, and secure gateways to process transactions.

These systems are widely used in e-commerce, mobile banking, and retail stores, making transactions quicker and more reliable. In fact, global digital payment transactions are expected to reach $14.79 trillion by 2027, showing how rapidly people are shifting toward digital payment methods.

Types of Electronic Payment Methods

Electronic payments come in several forms, each offering different benefits and suited for different contexts. Here are some of the most common types:

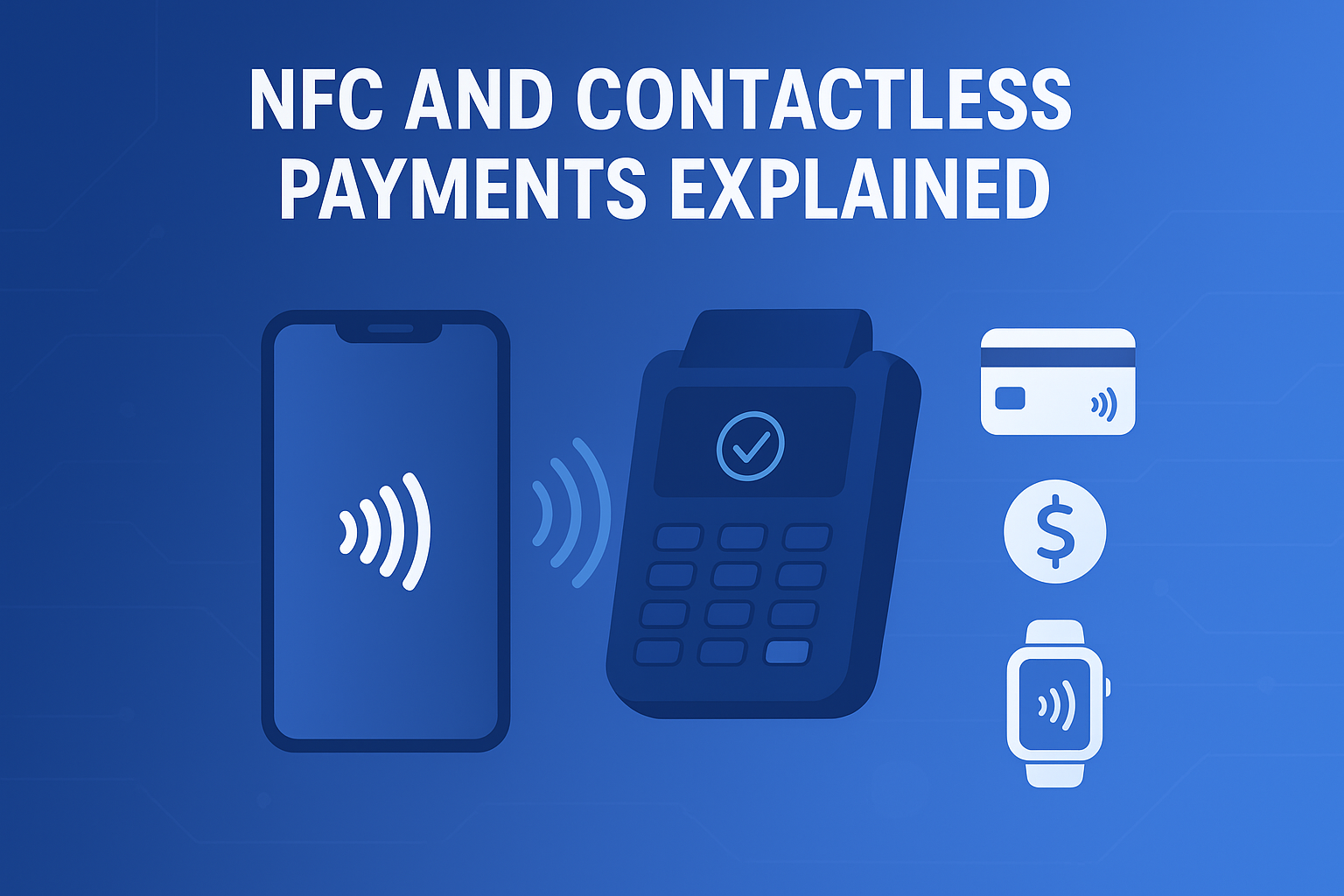

1. Contactless Payments

Contactless payments use technologies like NFC (Near Field Communication) or RFID (Radio Frequency Identification). Consumers can simply tap their debit or credit card, or even their smartphone or smartwatch, on a payment terminal to complete a purchase.

They’re not only fast but also highly secure since the card information is encrypted and tokenized, reducing the risk of fraud. Many payment processing solutions now integrate contactless options to improve user experience.

2. Internet Banking Payments

Internet banking allows users to make payments directly from their bank accounts using online banking portals or apps. Common uses include transferring funds, paying utility bills, or shopping online.

It’s one of the most secure payment methods, as transactions are protected by encryption, multi-factor authentication, and secure banking protocols.

3. QR Code Payments

Quick Response (QR) code payments have become extremely popular, especially in small businesses and emerging markets. The payer scans the merchant’s QR code with their mobile device, enters the payment amount, and completes the transaction instantly.

It’s a simple and low-cost method, making it ideal for local vendors and businesses that prefer flexible payment processing solutions.

4. ACH Payments

Automated Clearing House (ACH) payments are electronic bank-to-bank transfers used primarily in the U.S. These include payroll deposits, bill payments, and business-to-business transactions.

ACH payments are reliable, cost-effective, and a preferred option for recurring payments like subscriptions or rent.

How Do Electronic Payment Systems Work?

Electronic payment systems function through a series of digital steps that ensure the transaction is secure, verified, and successfully completed. Let’s break it down:

Step 1: Initiation

The process starts when the payer chooses a payment method—such as a credit card, mobile wallet, or online banking portal- and enters their payment information. This could happen online (e.g., during checkout on an e-commerce site) or in person (e.g., tapping a contactless card).

Step 2: Authentication

Once initiated, the system verifies the payer’s identity to prevent fraud. Authentication can involve passwords, one-time PINs (OTPs), biometrics, or security tokens. For example, two-factor authentication (2FA) has become a common layer of protection in most payment processing solutions.

Step 3: Authorization

After authentication, the payment gateway communicates with the payer’s bank or financial institution to confirm that the account has sufficient funds and is authorized for the transaction.

If everything checks out, the system approves the payment request and reserves the amount for processing.

Step 4: Processing

At this stage, the transaction is routed through secure networks between the payer’s and receiver’s financial institutions. The payment processor plays a vital role here, ensuring that sensitive data is encrypted and transferred safely.

According to a recent study, over 87% of global consumers now use digital payment methods regularly for purchases, reinforcing how secure and convenient these systems have become (source).

Step 5: Completion

Finally, the payment is confirmed, and both parties receive notifications of the successful transaction. The merchant’s account is credited, and the payer’s account is debited accordingly. Depending on the type of transaction, completion can occur instantly or within a few business days (as in ACH transfers).

The Benefits of Electronic Payment Systems

- Electronic payment systems bring multiple advantages for both businesses and consumers:

- Speed and Convenience: Instant transactions mean faster service and fewer delays.

- Enhanced Security: Encryption, tokenization, and authentication protect users from fraud.

- Global Accessibility: Users can send and receive money across borders effortlessly.

- Cost Efficiency: Reduces the cost of handling cash and check processing.

Integration with Business Tools: Many payment processing solutions integrate directly with accounting software, helping businesses manage their finances efficiently.

Conclusion

Electronic payment systems have transformed the way we transact, replacing cash-heavy operations with efficient, secure, and global digital solutions. Whether it’s tapping your phone at checkout, transferring money online, or paying through ACH, the variety of payment methods available today ensures that everyone can find a system suited to their needs.

As technology evolves, payment processing solutions will also advance, providing faster, safer, and more innovative ways to manage our financial lives. Businesses that adopt these systems not only improve customer experience but also stay competitive in a world rapidly moving toward a cashless future.