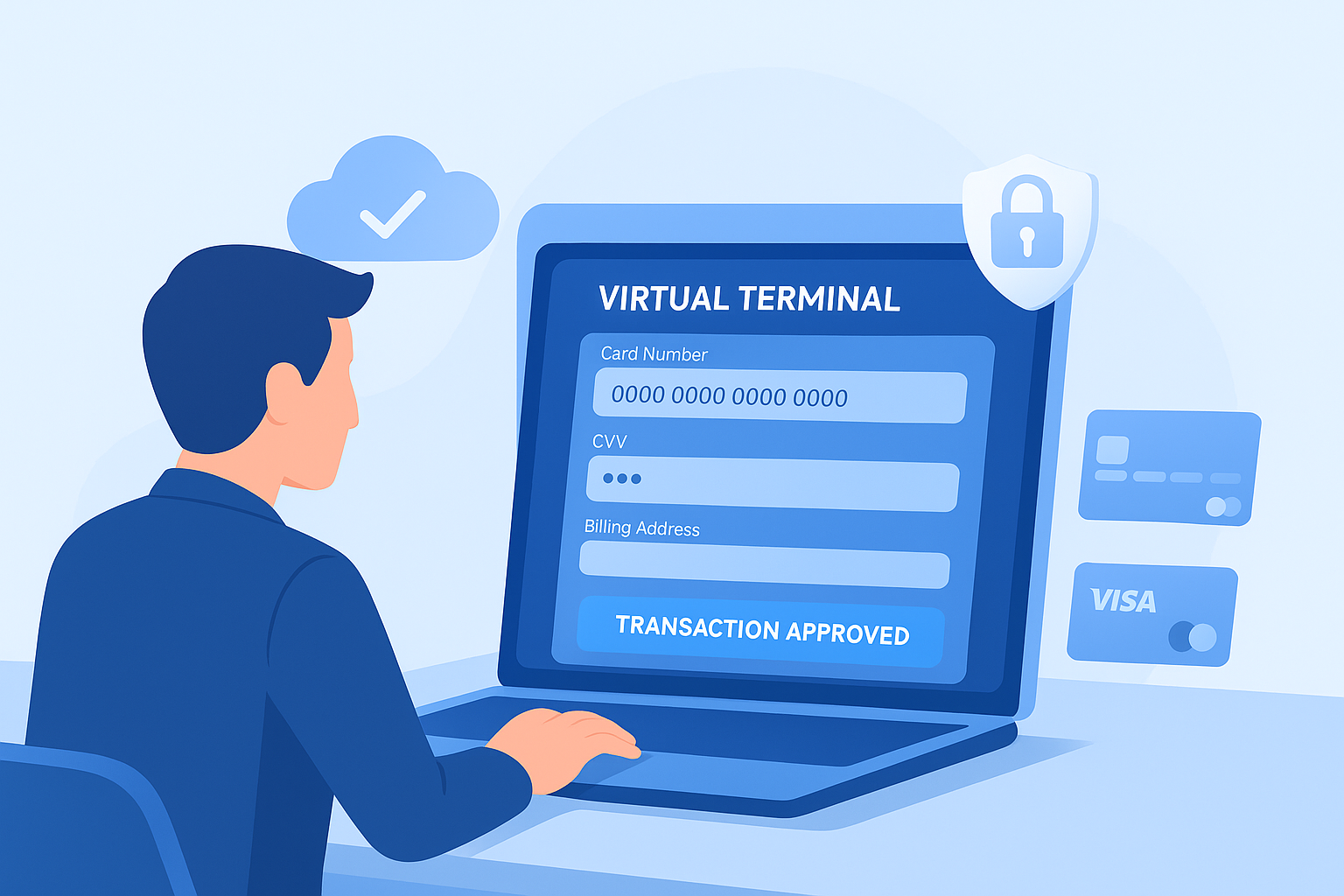

When you hear “virtual terminal,” don’t picture a physical card swiper or POS device. A virtual terminal is a software interface (usually web-based) that enables a merchant to manually enter a customer’s credit or debit card information to process a transaction, even when the card is not physically present. In short, you accept a card payment via your computer, tablet, or phone by typing in the card number, expiration date, CVV, etc.

Unlike a physical POS terminal, there’s no card swipe or insertion. This makes virtual terminals ideal for “card-not-present” situations: phone orders, mail orders, or remote payments.

The concept fits under the broader umbrella of payment processing solutions, because virtual terminal services are one tool among many that help a business accept payments securely and flexibly.

How Does a Virtual Terminal Work?

Here’s a step-by-step of how a virtual terminal processes a transaction:

Login / Access

The merchant logs into the virtual terminal dashboard (often provided by the payment processor or gateway).

Enter Payment Details

The merchant or operator types in the customer’s card number, expiration date, CVV (card security code), billing address, and amount to charge.

Send Authorization Request

Once submitted, the virtual terminal sends the transaction request securely over the internet to the payment processor (or acquiring bank).

Processor & Card Network Communication

The payment processor forwards the authorization request through card networks (Visa, Mastercard, etc.) to the issuing bank to check:

- Is the card valid?

- Is there enough credit or funds?

- Has fraud occurred?

Authorization Response

The issuing bank responds with either approval or a decline. This response propagates back to the merchant via the processor/cloud.

Capture / Settlement

If approved, the processor ultimately captures the funds and eventually settles them into the merchant’s bank account (usually within 1-3 business days, depending on the processor and banking rails).

Receipt / Confirmation

The merchant can generate a receipt (digital or printed) and send it to the customer.

Because the card never physically interacts with the merchant, extra security and verification (like CVV checks, address verification, and tokenization) are typically enforced to reduce fraud risk.

According to Helcim, virtual terminals account for 62.55% of total online transactions in certain markets, i.e., a dominant share of non-POS payment activity.

Thus, the virtual terminal process is relatively straightforward, but behind the scenes, it integrates with the same payment rails, networks, and fraud controls as any other form of card acceptance.

What Do You Need to Use a Virtual Terminal?

To get up and running, here are the usual requirements:

Merchant Account / Payment Processor

You must already have (or sign up for) a merchant account or a relationship with a payment processor or gateway that offers virtual terminal capabilities. Many modern processors bundle virtual terminal options with their standard services.

Internet-Connected Device

Any computer, tablet, or smartphone with a browser (or app) will work, as long as you can securely access the virtual terminal interface.

Security & Compliance

- The virtual terminal provider must be PCI-DSS (Payment Card Industry Data Security Standard) compliant.

- Data encryption, tokenization, and secure login credentials (2FA) are highly recommended.

- You may need to maintain compliance practices (e.g., never store full card data unless permitted, etc.).

Card Information From Customer

You need the card data (number, expiry, CVV, billing address). In many cases, the customer must supply the CVV and possibly address verification data.

Software Access / Credentials

The processor provides you access to their portal (username, password, sometimes roles or permissions).

Optional Integrations

Though not strictly required, many merchants integrate the virtual terminal with their CRM, invoicing software, or accounting systems to automate reconciliation and record-keeping.

Once you have the above, you can begin accepting payments via the virtual terminal just as you would via a physical point-of-sale systems, though the workflow is manual.

What Are the Benefits of a Virtual Terminal?

Using a virtual terminal offers several key advantages, especially in the right business context:

Flexibility & Remote Capability

You can accept payments anywhere you have internet, in your office, at home, or on the go, without installing hardware.

No Physical Hardware Cost

You don’t need to invest in card readers, POS terminals, or specialized devices. That reduces upfront costs and maintenance.

Ideal for Remote / Phone / Mail Order Sales

If your business takes phone orders, remote bookings, or mail orders, the virtual terminal is indispensable.

Lower Barriers to Entry

Small businesses or startups can begin accepting card payments without significant hardware investment.

Centralized Management

Transactions from various remote sources can be managed through one dashboard. It simplifies reporting and reconciliation.

Better Fraud Controls (if implemented well)

Because the provider handles encryption, tokenization, AVS (Address Verification Service), and other security measures, you often benefit from robust fraud defenses.

Scalability

You can add users, terminals, or integrations easily without physical infrastructure changes.

Support for Recurring / Stored Payments

Many virtual terminal solutions support storing a tokenized payment method for future charges (with consent), enabling recurring billing.

Because virtual terminals form part of payment processing solutions, they behave as a flexible layer that enables your business to accept card payments in virtually any environment.

What Businesses Should Use a Virtual Terminal?

A virtual terminal is a good fit for many business types, particularly ones where card-present sales are less common or practical:

- Service providers (consultants, contractors, repair services, freelancers) often take payments after the service or remotely.

- Call centers/phone order businesses where customers place orders by phone.

- Subscription/membership businesses that need to charge recurring payments.

- Nonprofits/charities taking donations over the phone or via mail campaigns.

- Medical, legal, and professional services that invoice clients and then accept payments remotely.

- E-commerce merchants who want a fallback for manual order entry or for dealing with order corrections by phone.

- Remote/offsite sales field agents, traveling salespeople, and delivery services.

- Startups or small businesses that prefer to avoid heavy hardware investment initially.

In short, if your business ever needs to accept card payments without having the physical card in hand (or when the card reader is not available), a virtual terminal is a strong option.

Conclusion

A virtual terminal is a powerful component of payment processing solutions, offering the ability to accept credit and debit card payments without needing physical hardware. It works by manually entering card details into a secure portal, which communicates with payment processors and card networks to authorize, capture, and settle funds.

To use one, you simply need a merchant account or payment processor that offers the service, an internet-connected device, and proper security compliance. The benefits include flexibility, low hardware cost, remote capability, and seamless management. Any business that takes orders over the phone, handles remote payments, or issues invoices can benefit from using a virtual terminal.